In the dynamic landscape of corporate governance, Corporate Sustainability Reporting Directive (CSRD) has emerged as a new requirement for reporting. The directive aims to provide stakeholders with a transparent view of a company’s social and environmental impact. If your company is required to disclose and report, how should you prepare and organise yourself to be ready? This guide will explain how the process works and what factors to consider.

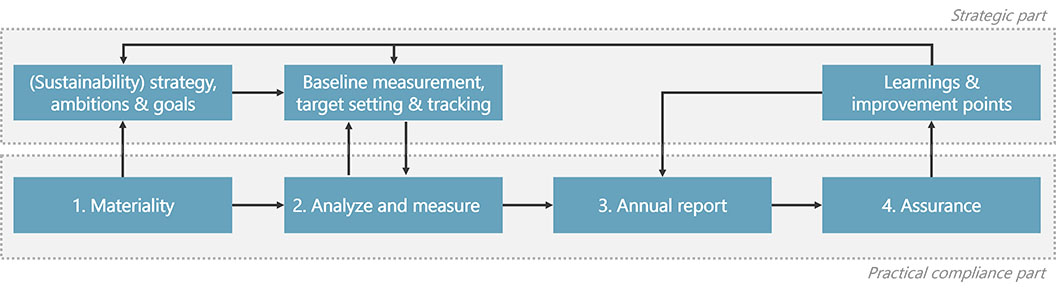

In our view CSRD implementation has two sides, the strategic and the practical. The strategic part deals with your ambitions, targets, and learnings, while the practical part zones in on developing the report for the financial reporting year. The diagram below outlines the elements that are included in each part.

Strategic Part

This segment deals with your company’s business strategy, focusing on ambitions, targets, and learnings, as well as sustainability across environmental, governance, and social topics. Together with your goals, this lays the groundwork for choices made later in the practical part. Don’t worry if everything isn’t worked out yet; the process will provide inputs for formulating a strategy later. Instead, what is important is to start making baseline measurements, such as GHG emissions. Calculating baseline Scope 1, 2, and 3 is a good way to start implementing CSRD.

Practical Compliance Part

1. Materiality

The starting point of the practical part of CSRD is the completion of a materiality assessment. This process is designed to select which ESG topics are material to your company’s situation. It involves performing a double materiality scan. This investigates two aspects, namely:

- Understanding the impact that your company’s operations have on its context (the inside out perspective).

- Risks and opportunities that influence your company’s operations (the outside looking in perspective).

This assessment covers all topics included in the EFRAG standards. The result is a materiality matrix and a document describing how you determined which topics are material. At this point, you know which disclosures to work on.

If you want to read more about conducting a double materiality assessment, visit our webpage about double materiality assessment.

2. Analyse and Measure

With the list of material disclosures clear, it’s time to investigate what needs to be reported in detail. New data points may need to be captured, as it is not always be possible to rely on existing enterprise data. Not all data will be quantitative; the CSRD includes many qualitative aspects. Consider your definitions and how the data can be captured again for the next year. This might mean setting specific KPIs or developing policies.

3. Annual Report

Once you are satisfied that all relevant information is available, it is time to develop the sustainability report. This should be a straightforward exercise aimed at disclosing the relevant information in accordance with the disclosure requirements.

4. Assurance

Once the report is finished, it needs to be audited with limited assurance. Any findings that result from the audit will be valuable input to use as learnings for improving your future reporting cycles.

How can Ecomatters help with CSRD?

With over 10 years of experience in sustainability reporting, Ecomatters offers the following services around CSRD implementation:

- Full CSRD implementation support across all steps in the above-described process.

- Materiality kick-start workshops to support starting with CSRD.

- Execution of the double materiality assessment.

- Calculation of Scope 1, 2, and 3 emissions using the Greenhouse Gas Protocol and assistance in quantifying other impacts.

- Provide support in organising data streams and identifying data gaps.

- Acting as an expert on certain topics.

If you want to discuss your project: plan a meeting with one of our experts

Services

Contact us

Max Sonnen

Eelco van IJken

Related articles

Call with our consultant

Do you want to know more about how we can help? Schedule a call with one of our consultants to ask your questions.